Home Renos – Tis the Season

Hello Summer. Hello Home Renovations... Most of us will [...]

Hello Summer. Hello Home Renovations... Most of us will [...]

During the COVID-19 pandemic, many Canadians from coast to coast [...]

Alta West Capital's Nomination We are proud to announce that [...]

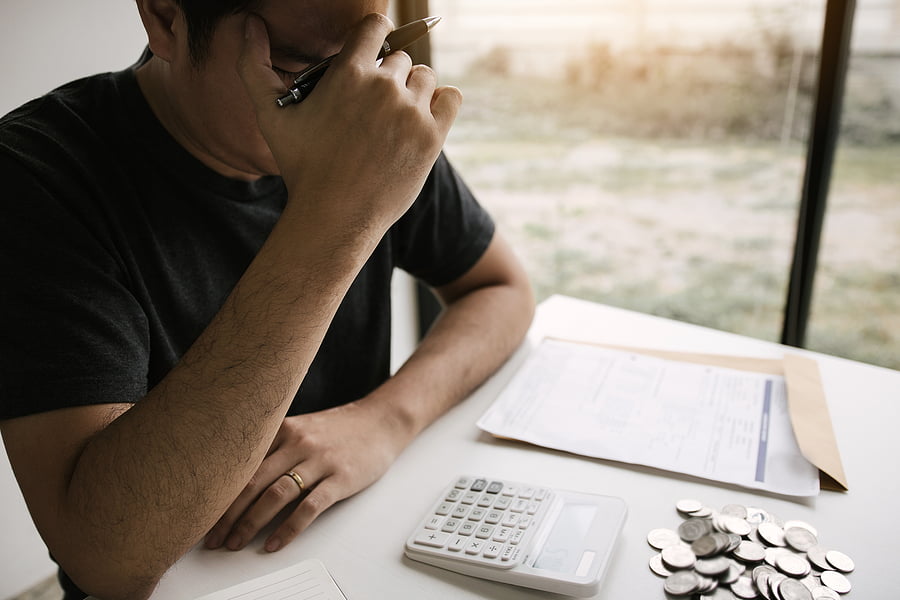

Financial Support The economic uncertainty caused by COVID-19 has impacted almost [...]

You’ve finally decided to take the plunge and start looking [...]

Most Canadians have some type of debt obligation, including one [...]

In today’s housing climate, mortgage pre-approval is a key element [...]

Advice From a Mortgage Investment Corporation When it comes [...]

Before spending money on a home renovation, you may want [...]

When it comes to making any significant financial decision, it’s [...]